A superbill is a detailed document provided by a healthcare provider that includes patient information, diagnosis codes (ICD 10), procedure codes (CPT), and charges, allowing patients to submit claims to their insurance for out-of-network reimbursement.

A superbill is a detailed summary of a patient visit that you give to the patient so they can submit it to their insurance for possible reimbursement. You do not file the claim. The patient does.

Superbills are not for every practice. They are not for every patient. But in the right situation, they save you from having to credential with dozens of insurance plans while still giving your patients a path to reimbursement.

This guide walks through what a superbill is, who uses it, what goes on it, and how to create one that actually gets paid. Superbills also play a critical role in overall revenue cycle management, particularly for out-of-network and cash-pay practices.

Key Takeaways

- Superbills are used for out-of-network reimbursement

- Patients submit claims, not providers

- Must include CPT, ICD 10, NPI, and charges

- Do not guarantee reimbursement

What Is a Superbill?

A superbill is a document that contains all the information an insurance company needs to process a claim. It is called a superbill because it is a “super” bill – more detailed than a standard receipt, less formal than a full claim submission.

The superbill serves as the source document for the patient’s claim. The patient takes the superbill, attaches it to a claim form (usually the CMS-1500), and sends it to their insurance company. The insurance company uses the information on the superbill to determine what they will reimburse.

How the Payment Flow Works

Here is the difference between standard billing and superbill billing.

Standard in-network billing:

- You provide service

- You submit claim to insurance

- Insurance pays you directly

- You bill patient for remaining balance

Superbill billing (out-of-network):

- You provide service

- Patient pays you in full at the time of service

- You give patient a superbill

- Patient submits superbill to their insurance

- Insurance reimburses patient directly (if they have out-of-network benefits)

You never file the claim yourself. The patient does. That is what makes a superbill different from standard billing.

When Should You Use a Superbill?

Use when:

– Out of network provider

– PPO plans

– Cash pay practices

Avoid when:

– In network provider

– Medicare or Medicaid patients

– No out of network benefits

How to Submit a Superbill to Insurance

Submitting a superbill correctly is essential for reimbursement. Since providers do not submit the claim, the responsibility lies with the patient.

Step-by-Step Process

- Complete a Claim Form (CMS-1500)

Patients must fill out a CMS-1500 form using the details provided on the superbill. - Attach the Superbill

The superbill acts as supporting documentation, including CPT codes, ICD-10 diagnosis codes, NPI, and charges. - Submit to Insurance Provider

Claims can be submitted through:- Online insurance portals

- Mail or fax

- Mobile apps (depending on payer)

- Track Claim Status

Patients should monitor claim processing through their insurer’s portal or customer service. - Review Explanation of Benefits (EOB)

The insurer will issue an EOB showing the allowed amount, reimbursement, and patient responsibility.

Missing or incorrect information can result in claim denial or delayed reimbursement.

How Insurance Reimbursement Works with a Superbill

Insurance reimbursement for superbills depends on several key factors defined by the patient’s plan.

Key Factors That Affect Payment

- Allowed Amount

The maximum amount the insurance company considers for a service, which is often lower than the billed charge. - Deductible

The amount the patient must pay out of pocket before insurance begins reimbursing. - Coinsurance

The percentage of the allowed amount the insurance pays after the deductible is met.

Example

If a provider charges $150 and the insurer’s allowed amount is $100:

- Patient may receive $70–$80 reimbursement depending on coinsurance

- Remaining amount is patient responsibility

A superbill does not guarantee full reimbursement, as the insurance policy determines payment.

Simple Example of a Superbill

A patient visits an out-of-network therapist and pays $150 at the time of service.

- The provider gives a superbill with CPT and ICD-10 codes

- The patient submits it to their insurance

- Insurance approves an allowed amount of $100

- After coinsurance, the patient receives $70 reimbursement

This process shows how superbills help patients recover part of their out-of-pocket costs.

What a Superbill Is Not

A superbill is not a receipt. A receipt just says “paid X amount on Y date.” A superbill includes clinical information such as diagnosis and procedure codes.

A superbill is not a claim form. A claim form is a standardized document (CMS-1500 or UB-04) that you submit to an insurance company. A superbill is the source document that the patient uses to fill out the claim form.

A superbill is not a substitute for a contract. Giving a patient a superbill does not mean you are in network with their insurance. It does not guarantee they will get reimbursed. It only gives them the information they need to try.

Superbill vs CMS-1500 Claim Form

| Feature | Superbill | CMS-1500 |

| Purpose | Provides billing details | Submits claim to insurance |

| Submitted by | Patient | Provider (or patient manually) |

| Format | Flexible document | Standardized form |

| Contains codes | Yes (CPT, ICD-10) | Yes (required fields) |

| Role | Source document | Official claim |

The superbill provides the information, while the CMS-1500 is the actual claim submission form.

Who Uses Superbills

Superbills are not for every practice. They are most useful for providers who do not contract with insurance companies directly.

Providers Who Commonly Use Superbills

- Independent practices not in network with insurance – These practices choose not to credential with insurers. They set their own fees. Patients pay cash or credit at the time of service. The practice gives a superbill so patients can seek out-of-network reimbursement.

- Direct primary care and concierge medicine offices – These practices charge a monthly or annual membership fee. They do not bill insurance for routine care. They provide superbills for patients who want to submit claims to their insurance for possible reimbursement.

- Cash-pay practices – Mental health providers, chiropractors, physical therapists, and other specialists often operate on a cash-pay basis. They are not credentialed with insurance companies. Patients pay up front. The provider gives a superbill.

- Providers who are not enrolled with specific payers – A provider might be enrolled with some payers but not others. For the payers they are not enrolled with, they use superbills.

- Out-of-network providers – Even if a provider is willing to take insurance, they might not have a contract with a specific patient’s plan. The patient chooses to see them anyway. The provider gives a superbill so the patient can file an out-of-network claim.

When a Superbill Does Not Make Sense

- In-network providers – If you are contracted with a patient’s insurance, you should file the claim directly. That is what your contract requires. Giving the patient a superbill instead of filing the claim yourself violates most payer contracts.

- Patients without out-of-network benefits – If the patient’s plan does not cover out-of-network care, a superbill is useless. They will get zero reimbursement. You need to confirm out-of-network benefits before promising anything.

- Medicare and Medicaid patients – These programs have strict rules about balance billing and out-of-network coverage. In most cases, you cannot give a Medicare or Medicaid patient a superbill and expect them to file it themselves. You either enroll in the program and bill directly, or you do not treat those patients.

Who Needs a Superbill

Not every patient who sees an out-of-network provider needs a superbill. The superbill is only useful for patients who plan to seek reimbursement from their insurance.

Patients Who Should Get a Superbill

- Patients with PPO plans that include out-of-network benefits – PPO plans typically cover out-of-network care at a lower percentage than in-network care. The patient pays you up front, then files a claim to get back whatever their plan allows.

- Patients with out-of-network coverage through their employer – Some employer-sponsored plans offer out-of-network benefits even if the plan is not a traditional PPO. Check the patient’s summary of benefits.

- Patients with health savings accounts (HSAs) – Patients with HSAs may need a superbill to substantiate HSA distributions, even if their insurance does not reimburse them. The IRS requires documentation for HSA withdrawals.

- Patients who pay out of pocket and want to track medical expenses for taxes – Even without insurance reimbursement, patients may want a superbill to document medical expenses for tax deductions.

Patients Who Do Not Need a Superbill

- Patients who are not seeking reimbursement – Some patients pay cash and do not bother filing insurance claims. They do not need a superbill. A simple receipt is fine.

- Patients with HMO plans – HMO plans generally do not cover out-of-network care except for emergencies. A superbill will not help them.

- Patients with no out-of-network benefits – If the patient’s plan explicitly excludes out-of-network coverage, a superbill is worthless. The insurance company will deny the claim.

- Patients whose deductible is far from being met – Even with out-of-network coverage, the patient pays the full allowed amount until they meet their deductible. If their deductible is $5,000 and they have only spent $500, they will get nothing back from a $200 visit.

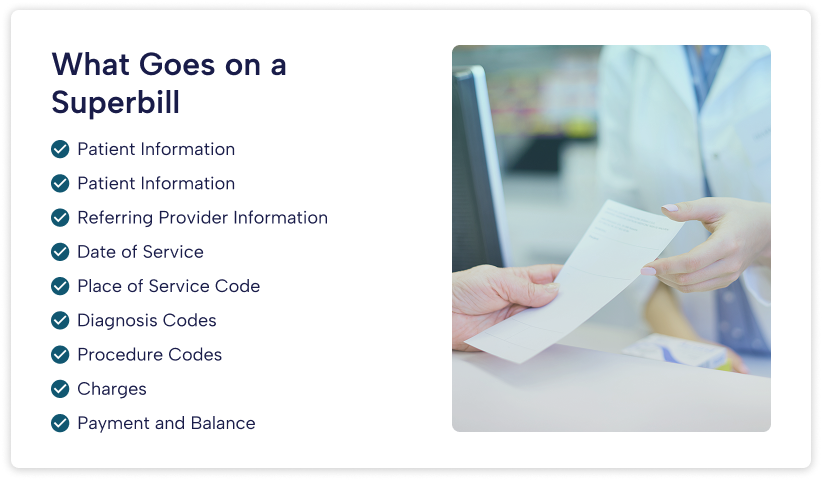

What Goes on a Superbill

A superbill contains all the information an insurance company needs to evaluate a claim. If you leave something out, the patient’s claim gets rejected. Here is exactly what you need to include.

Provider Information

The insurance company needs to know who provided the service.

- Provider’s full legal name (as registered with Medicare or the state)

- Provider’s National Provider Identifier (NPI) number

- Provider’s credentials (MD, DO, NP, PA, etc.)

- Practice name (DBA if different from legal name)

- Practice address (physical location, not a PO box)

- Practice phone number

- Tax Identification Number (EIN or SSN)

Patient Information

The insurance company needs to identify the patient and match them to their policy.

- Patient’s full legal name (must match insurance card exactly)

- Patient’s date of birth

- Patient’s address

- Patient’s insurance ID number (as shown on their card)

- Patient’s group number (if applicable)

- Patient’s relationship to the subscriber (self, spouse, dependent)

Referring Provider Information

If the service required a referral, include the referring provider’s information.

- Referring to the provider’s full name

- Referring provider’s NPI

- Referring to the provider’s credentials

Date of Service

The specific date the service was provided. Use MM/DD/YYYY format.

If the service spanned multiple days (like a hospital stay), include the start date and end date.

Place of Service Code

A two-digit code that tells the insurance company where the service happened.

- 11 – Office

- 12 – Home

- 21 – Inpatient hospital

- 22 – Outpatient hospital

- 23 – Emergency room

- 24 – Ambulatory surgical center

- 31 – Skilled nursing facility

Use the wrong code, and the claim gets denied. A service provided in your office is coded 11. The same service provided in a hospital outpatient department is coded 22. Reimbursement rates differ significantly.

Diagnosis Codes

ICD-10-CM codes that describe the patient’s condition. Include the full code, not just the first three characters.

- List the primary diagnosis first (the main reason for the visit)

- List additional diagnoses that were addressed or that support medical necessity

- Do not include diagnoses that are not relevant to the visit

Each diagnosis code must be valid for the date of service. Codes change every October. Using a code that was deleted last year gets the claim rejected.

Procedure Codes

CPT or HCPCS Level II codes that describe what you did.

- CPT codes for evaluation and management, procedures, and testing

- HCPCS Level II codes for supplies, drugs, and equipment

Include modifiers where required. Modifiers tell the insurance company about special circumstances. For example, modifier 25 means a significant, separately identifiable evaluation and management service was provided on the same day as a procedure.

Each procedure code must be linked to the diagnosis code that supports it. This is called a diagnosis pointer. The superbill should show which diagnosis goes with which procedure.

Charges

The amount you charged for each service. List each service separately. Do not lump multiple services into one line.

- Charge for the office visit

- Charge for each procedure

- Charge for any supplies or drugs

The charge is what you billed, not what you expect to be paid. Out-of-network reimbursement is based on the insurance company’s allowed amount, which is usually lower than your charge. That is fine. The patient needs to see your charge on the superbill.

Payment and Balance

The amount the patient paid at the time of service.

- Total charges

- Amount paid

- Remaining balance (should be zero if the patient paid in full)

Insurance companies want to know that the patient paid you. They will not reimburse the patient for amounts they did not pay.

How to Create a Superbill That Actually Works

Creating a superbill is not complicated, but it must be accurate. Errors get claims denied. Denied claims mean angry patients.

You can also follow a structured medical billing audit checklist to ensure accuracy, compliance, and complete documentation before issuing superbills.

Use Standardized Codes

Do not write descriptions in plain English. Insurance companies do not read plain English. They read codes.

Wrong: “Extended office visit with patient with diabetes.”

Right: “99214” with diagnosis code “E11.9”

Wrong: “Therapy session for anxiety.”

Right: “90837” with diagnosis code “F41.1”

If you do not use standard codes, the insurance company cannot process the claim. They will send it back to the patient and ask for corrected codes. Most patients do not know how to fix this. They give up. You lose a referral source.

Link Diagnosis Codes to Procedure Codes

Every procedure code needs a diagnosis code that supports it. This is called medical necessity. The insurance company will not pay for a procedure if the diagnosis does not justify it.

Example:

- Procedure: 99214 (office visit, established patient, level 4)

- Diagnosis: M17.9 (osteoarthritis of knee, unspecified)

The diagnosis supports the procedure. The patient came in for knee pain. You evaluated them. That is a valid visit.

Now imagine this:

- Procedure: 99214

- Diagnosis: Z01.89 (encounter for other specified special examination)

The diagnosis does not support a level 4 visit. The patient came in for a routine check-up. A level 4 visit is for patients with moderate to high complexity. The claim will deny.

Your superbill needs to show which diagnosis goes with which procedure. Most superbills use a grid or a numbering system. List each diagnosis with a number (1, 2, 3). Next to each procedure, list the numbers of the diagnoses that support it.

Include NPI Numbers Correctly

Insurance companies expect to see two NPIs on a claim.

- Rendering provider NPI – The individual provider who actually saw the patient. This is usually an individual NPI (type 1).

- Billing provider NPI – The practice or organization that bills for the service. This is usually an organizational NPI (type 2).

If you are a solo practitioner, these may be the same. If you work in a group, they are different. Use the wrong one and the claim gets rejected.

Check the Date of Service

The date of service must be exactly right. If you saw the patient on March 15, put March 15. Do not put March 16. Do not put March 14.

If the service spanned multiple days, put the start date and end date. For a hospital stay, put the admission date and discharge date.

If the patient had multiple services on different dates, list each date separately. Do not lump them together.

Verify Patient Information Before Printing

Before you hand a patient a superbill, verify that the patient’s information is correct. Ask them to confirm:

- Their full legal name as it appears on their insurance card

- Their date of birth

- Their insurance ID number

Do not assume the information in your system is current. Patients change jobs. They get divorced. They turn 65 and switch to Medicare. Verify at every visit.

Electronic Superbills vs. Paper Superbills

Paper Superbills

Paper superbills are exactly what they sound like. You print a document and give it to the patient.

Advantages:

- No technology required. Any practice can do it.

- Patient leaves with the document in hand. No waiting.

- Works for every patient regardless of their technical ability.

Disadvantages:

- Paper gets lost. Patients put it in a drawer and forget about it.

- Handwriting can be illegible. If the insurance company cannot read the codes, they deny the claim.

- No built-in validation. You can put invalid codes on a paper superbill without realizing it.

- Patients have to mail or fax the superbill to their insurance company. That adds days or weeks.

Electronic Superbills

An electronic superbill is a digital file, usually a PDF, that you email to the patient or make available through a patient portal.

Advantages:

- Cannot be lost. The patient can always download another copy.

- Legible every time. No handwriting issues.

- Can include validation. Your billing software can check that codes are valid before you generate the superbill.

- Patients can upload the PDF directly to their insurance company’s claim portal. Faster processing.

Disadvantages:

- Requires technology. You need billing software that can generate electronic superbills.

- Requires the patient to have email or portal access. Some patients do not.

- Patients may not check their email or portal promptly. They might not realize the superbill is available.

Most practices today use electronic superbills. The technology is standard in most billing software. If your software does not generate superbills, consider upgrading.

Common Superbill Mistakes That Get Claims Denied

Here are the most common errors I see on superbills. Each one leads to a denied claim and an angry patient. Many of these errors also contribute to claim rejections in medical billing, especially when incomplete or incorrect data is submitted.

Mistake 1: Missing or Incorrect NPI

The rendering provider NPI is missing. Or you used the group NPI when the payer expects the individual NPI. Or you used an NPI that is not enrolled with the payer.

Fix – Always include both NPIs. Verify that each NPI is active and correct for the payer.

Mistake 2: Invalid Diagnosis Code

You used an ICD-10 code that does not exist. Or you used a code that was deleted in the last annual update. Or you used a code that is not valid for the patient’s age or gender.

Fix – Use a current ICD-10 code book or software. Update your codes every October.

Mistake 3: Unbundled Codes

You billed separately for services that should be bundled together. For example, billing for a routine office visit on the same day as a preventive medicine visit without using the correct modifier.

Fix – Learn the bundling rules for the codes you use most often. Use modifiers when appropriate.

Mistake 4: Missing Modifiers

The procedure code requires a modifier, but you left it off. For example, billing for a bilateral procedure without modifier 50.

Fix – Check payer requirements for each procedure code. Some require modifiers. Some do not. Know the difference.

Mistake 5: No Diagnosis Link

You listed procedure codes, but did not show which diagnosis supports each procedure. The insurance company has no way to assess medical necessity.

Fix – Use a superbill format that includes diagnosis pointers. Number each diagnosis. Next to each procedure, list the numbers of the diagnoses that support it.

Mistake 6: Wrong Place of Service Code

You coded an office visit as place of service 11 when it should be 22. Or you coded a telehealth visit as 11 instead of 02.

Fix – Know the correct POS code for every service location. Update your codes when telehealth rules change.

These issues often result in specific denial codes from payers, which indicate why a claim was rejected or not reimbursed.

Legal and Compliance Considerations

Balance Billing Rules

A superbill does not change your obligation under balance billing laws. If you are in network with a patient’s insurance, you cannot give them a superbill and bill them your full fee. You must bill the insurance directly and accept the contracted rate.

If you are out of network, you can bill the patient your full fee. The superbill is just documentation. But some states have balance billing protections for out-of-network emergency care and certain other services. Know your state’s rules.

Fraud and Abuse

Do not put false information on a superbill. Do not upcode (bill for a higher level of service than you provided). Do not unbundle (bill separately for services that should be bundled). Do not bill for services you did not provide.

Insurance companies audit out-of-network claims just like in-network claims. If they find fraud on a superbill, they can pursue you for damages. They can also report you to state licensing boards and the OIG.

Good Faith Estimates

Starting in 2022, the No Surprises Act requires providers to give uninsured and self-pay patients a good faith estimate of charges before providing services. A superbill is not a substitute for a good-faith estimate. You must provide the estimate separately.

If you treat self-pay patients, learn the good faith estimate requirements. The penalties for non-compliance are steep.

Quick Summary

A superbill is a detailed billing document that allows patients to submit out-of-network claims using standardized codes such as CPT and ICD-10. It includes provider information, patient details, and service charges, helping insurers determine reimbursement based on policy terms.

Conclusion

A superbill is a tool. It lets you serve patients even when you are not in network with their insurance. The patient pays you up front. You give them a superbill. They file for reimbursement themselves.

Superbills work best for out-of-network providers, direct primary care practices, cash-pay practices, and patients with PPO plans that include out-of-network benefits.

To create a superbill that actually gets paid, include accurate provider and patient information, valid diagnosis codes, correct procedure codes with modifiers, proper diagnosis links, and complete charge information. Use electronic superbills when possible. Train your staff on common mistakes.

And remember. A superbill does not guarantee reimbursement. The patient still needs to file the claim correctly. Their plan still needs to have out-of-network benefits. Their deductible still applies. Set realistic expectations up front. Tell patients what to expect. Give them instructions. Answer their questions.

FAQs

What is a superbill used for?

A superbill is used to help patients submit out of network claims for reimbursement. It contains all the coding and provider details required by insurance companies to process the claim.

Does a superbill guarantee reimbursement?

No, reimbursement depends on the patient’s insurance benefits, deductible, and out of network coverage. The superbill only provides the required information.

Who submits a superbill?

The patient submits the superbill to their insurance company. The provider does not file the claim in this process.

Can Medicare patients use superbills?

In most cases, Medicare patients cannot use superbills for reimbursement due to strict billing rules. Providers must follow Medicare billing requirements directly.

Simplify Your Billing Process with Expert Support

Managing superbills, coding, and reimbursement can get complicated fast. Small errors lead to denied claims, frustrated patients, and lost revenue.

Medhasty helps you handle billing the right way. From accurate coding to clean documentation and fewer rejections, you get a smoother workflow and better financial outcomes.

If you want fewer billing headaches and more predictable revenue, it’s time to bring in the right support.

Talk to Our Medical Billing Expert